transitory?

market vibes

“You are what you eat.” Anthelme Brillat-Savarin, 1826

A slew of data this week, including JOLTS, Q1 GDP, ADP, PCE inflation, ISM, and Non-Farm Payrolls. Plus, approximately 180 S&P 500 companies will report this week (40% of market cap), including Apple, Microsoft, Amazon, and Meta. Since there’s a dearth of weekend news news, I’ll share a few random thoughts this morning:

The President attended the Pope’s funeral and wore a blue suit. His use of fashion was, I think, a statement. While in Rome, Macron attempted to join a private Trump-Zelensky tête-à-tête and was told “no.”

In tariff-world, LVMH is in the ditch, ostensibly due to Chinese knock-offs (ironic, lol!). Frankly, I think LVMH is suffering because Ukrainian buyers for Birkin bags tapped out when Trump cut them off.

Maria Bartiromo said on her Sunday show that “Trump’s tariffs have already added $5 billion per day in new revenues. In other words, the one-trillion/year trade deficit is gone.” I will add, that’s $5 billion a day we don’t have to borrow. I’m thinking about bonds.

In the markets

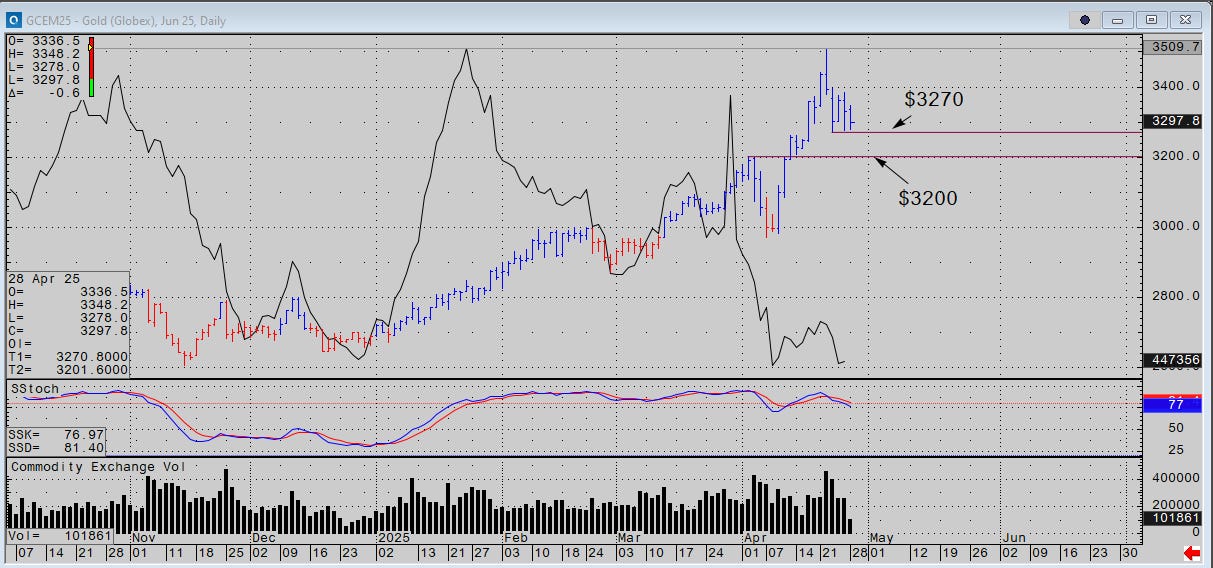

Gold popped above the $3340 POC after the close on Friday and opened higher last night into stiff resistance. Gold trades heavy, perhaps because the millions of ounces sold last week are still sloshing around in the range. At the moment, prices may test $3270. However, the POC at $3340 is an active force, so anyone thinking of a short sale should be patient and sell it as close to the POC as possible.

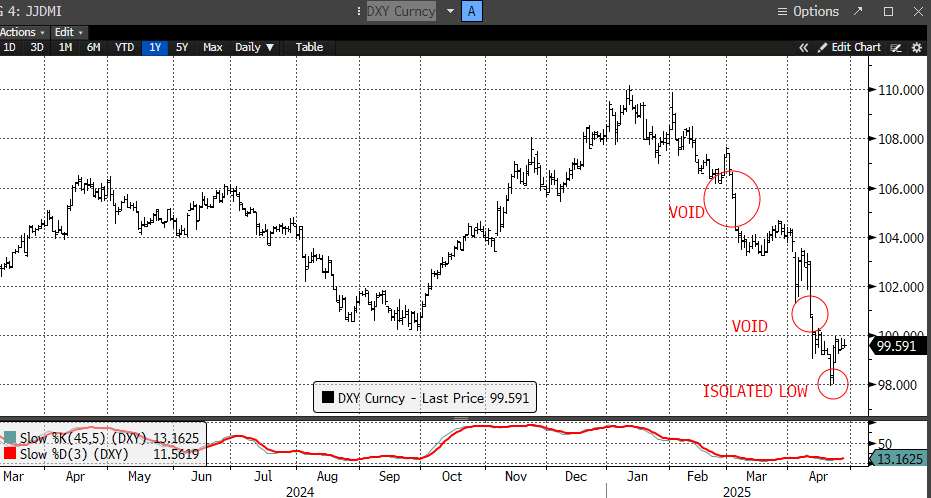

I wouldn’t sell gold under $3300 unless it’s under $3270 and DXY is pushing into the void (chart below). The bear narrative would be lower gold, higher USD, higher bonds and stocks, good earnings, good tariff news, etc. A few “good” logs on the fire that will burn.

In my opinion, Q1 earnings are pre-tariff but Q2 earnings will be critical. With Federal debt at 39 tirillion in the visible future, a rally in DXY is going to be pretty small beer. Once the markets acept tariffs are a tax (not inflation), bonds could rally. The best case for S&Ps is a range below the 200 D MA which is where something like 50% of stocks already are this morning. Recession? You decide.

Moving along with oil, bonds silver and bitcoin this morning, it’s very low and slow, steady as she goes…