low hanging fruit

April 23…)

in the news

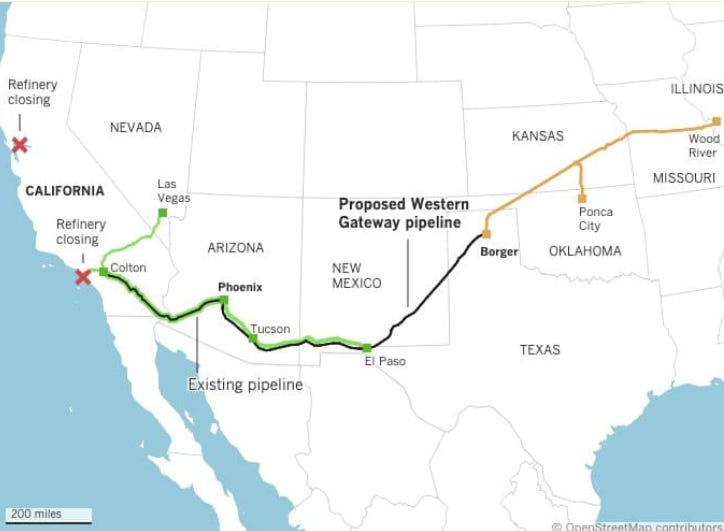

Phillips 66 and Kinder Morgan say they have enough commitments to build a pipeline from Arizona to the west coast. Today, California is almost entirely dependent on seaborne imports of crude and fuel.

Brazil posted a record trade surplus of $14.2 billion in the first quarter; crude oil exports rose 31% Y/Y to $12.56 billion with 57% going to China (65% in March alone). BBG reports 29 VLCCs have been denied transit at the Strait as “Tehran (wtf?) Keeps The Strait Shut.”

China has been “aggressive sellers” of oil in the last 2 weeks. Asia is laden with the largest inventories of physical oil on the planet. If Asian reserves were not so incredibly immense, oil would have rallied from $30/barrel to $60 instead of from $60/barrel to $119.00… immho… As for China profit taking … Good trading!

BLS employment data came in unchanged as usual this morning. There was a time when the mind of the market was attentive to data produced by literally thousands of Federal economists and PhDs. Not any more. The mind of the market watches gold, silver, oil, stocks and their uncertain future. More on that in the Vibe this morning.

in the markets

Oil prices are moving horizontally in extremely light volume and liquidating open interest. Just as Iran has no cogent or cohesive voice with which to speak to the world, the facts and misinformation in oil has become so cacophonous and blatantly wrong the mind of the market simply ignores it.

Oil is a squeezeless silver with a much shorter cycle meaning… over-hyped lies and data, notorious unchecked front running (China?), fake narratives and a complete vacuum of trust because prices refuse to validate the hype. Just when you think faith in oil as an investable asset can’t go lower… it goes lower.

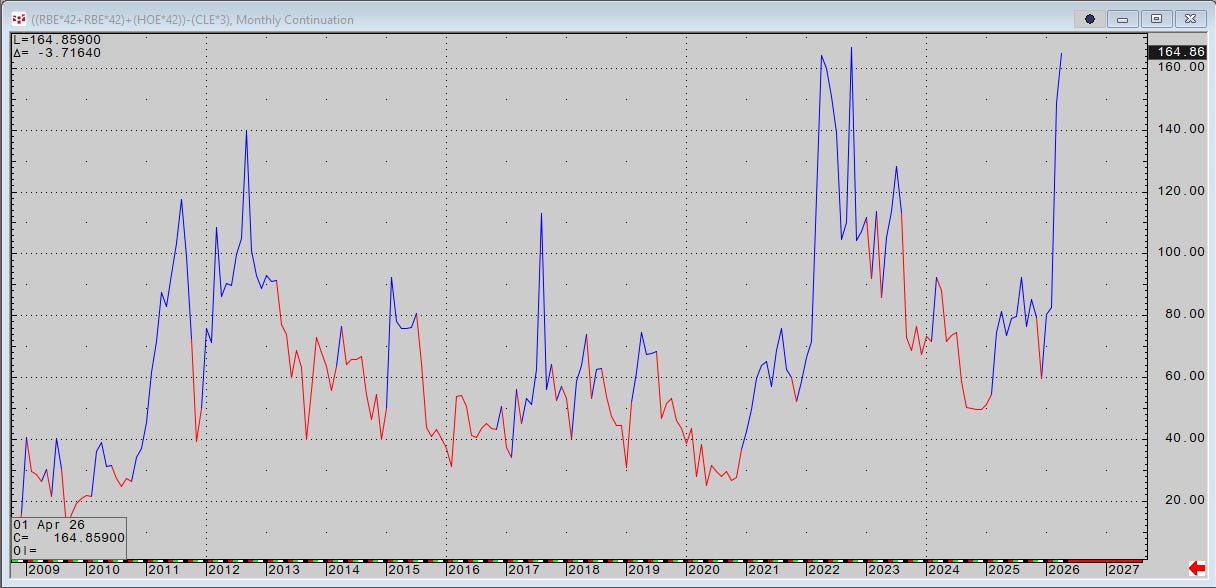

On the other hand… refinery margins have yet to exceed all time highs but a few more refinery fires and the chart below will sprint to another record! Or not …depending on Trump and Iran… and there it is.

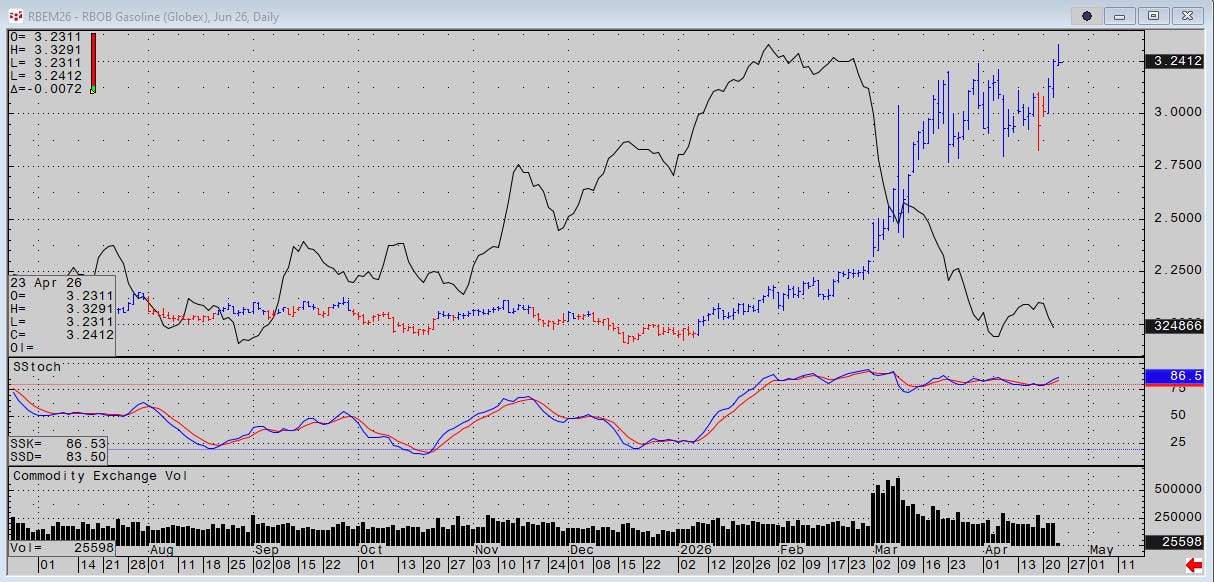

June rbob made new contract highs yesterday on falling OI and light volume… yet still nominally 10% lower than its June 2022 highs.

NDX futures look and feel like the low hanging fruit has been picked. The narrative is almost exclusively “buy the dip” and the chart below implies “the fruit eaten at the mountain top etc.” but this could actually be the valley.