haditnotbeenfor

market vibes

“Had it not been for” is a negative condititional phrase. Had being the past perfect tense of the verb to have. Been is a participial modifier of had. The form omits the hypothetical if : “if it had not been for.”

Sometimes looking for a perfect word to say “looking back”, you have make one up. For the purposes of this essay, I would like the reader to consider haditnotbeenfor a single word. (hat tip, Mrs. Fowler, 7th grade Latin).

"This shows how liars are rewarded: even if they tell the truth, no one believes them." The boy who caled wolf! Aesop circa 600 BC

There’s been an obsessive preoccupation with a stock bubble since Yellen said, “run hot” years ago. Analysts like JPM’s Marko Kolanović at money-center banks were so bearish for so long that the banks finally fired them… years ago. They were wolf-calling like the boy in Aesop’s fable, and after years of false alarms, the clients stopped listening.

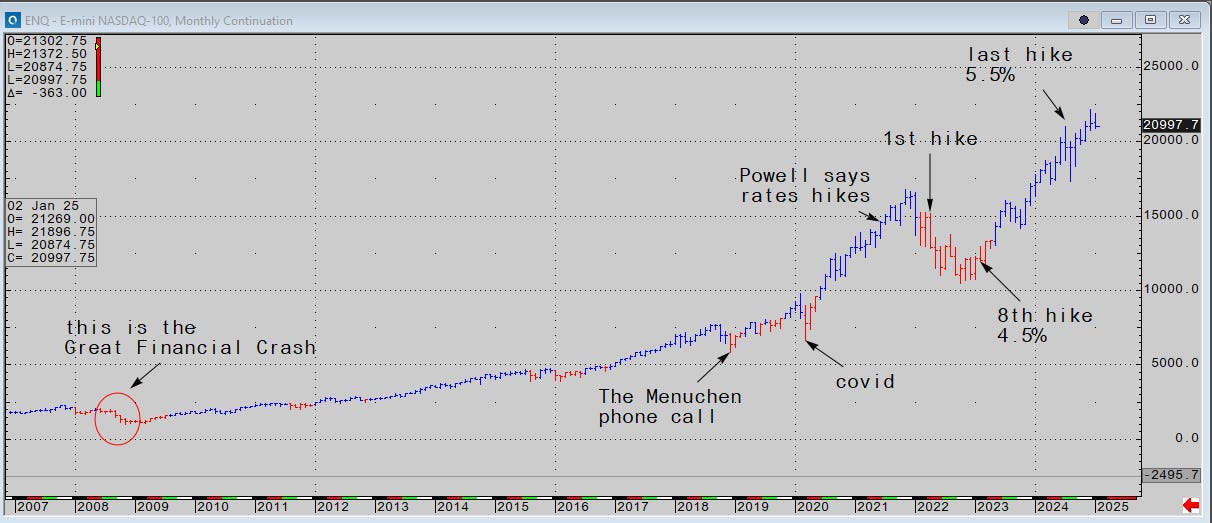

In the fall of 2017, put/call sentiment was so bearish you could sell a single December at-the-money S&P put and buy five at-the-money calls for zero cost. That’s how frothy the stock market was seven years ago. Scions and asset managers were on CNBC saying, “inflation is rising, the end is near.” Jay Powell caught the fever and started hiking rates saying, “We’re a long way from neutral” on October 3, 2018. He almost lost his job for it and backed off. By the end of Q1, 2019, he was cutting.

Sentiment is the gamma and volatility of narratives. However, not so in 2025. The facts are all bearish, but no one cares. Buffett has been flat for years. The market cap of ten U.S. stocks equals a fifth of all the stocks on Earth. No one cares! they tweet about it but … so what. Sell-side smart money on the Street was bullish into February as of last week.

Getting back to the chart at hand: as the FOMC added liquidity in 2020, stock prices tripled in two years. Then, in 2022, they dipped a tick to 20% as the FOMC hiked eight times in a single year, often at 0.75 bps per clip. Then, when Powell said, “not yet” in December 2022, meaning “soon,” stock prices bottomed and doubled in 15 months. Sure. Perfectly normal.

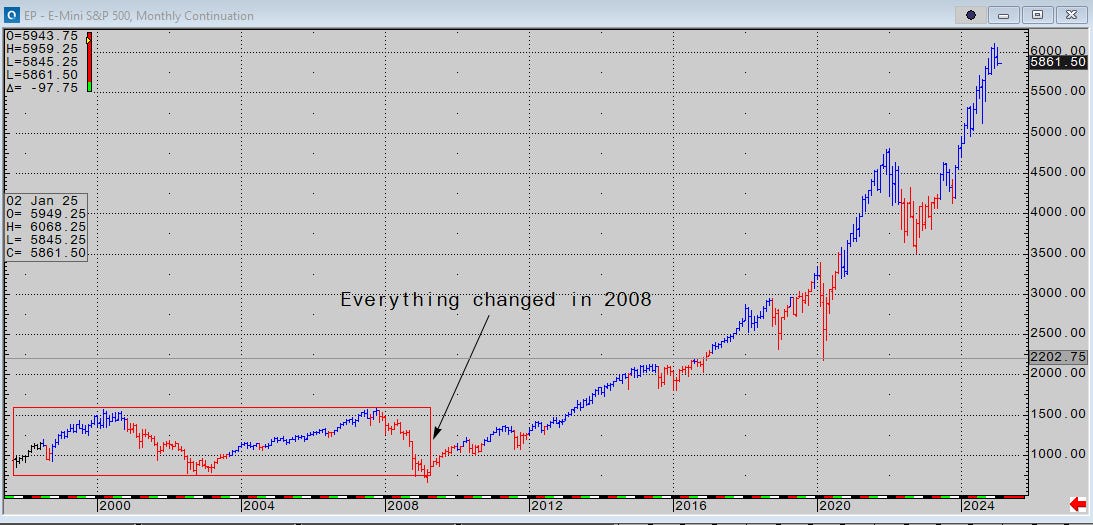

The first chart below is instructive: To the very far left, one can recognize the Great Financial Crash, a quaint iteration of financial stress. This chart is monthly data from the CQG database. The scale is correct. What your eyes are telling you is the “Great Crash” was a tiny blemish in a 40 year succession of events imposing vast amounts of borrowed money to stave off a succession of periodic contractions in leverage.

Every crisis enabled a transfer of wealth to the stock market. I would say these were more than a transfer of wealth. They were a transfer of power. American liberty was being slowily poisoned by leverage.

When Lehman collapsed, the narrative that households were incapable of managing their wealth (just as they’re incapable of doing their taxes) accelerated automated flows to the stock market. Households have always been the largest owners of equities and the economic recovery included a gradual cessation of wealth management to Wall Street. Submission or consent… Uncle! No mas.

Boomers, retirees, and investors had been terrorized by 1987 and the Y2K dot-com crash. Lehman was the coup de grâce. To wit: BlackRock, post pandemic, has $11 trillion AUM today. A handful of names have custody of 90% of the planet’s wealth. Three names have custodial control of 90% of U.S. stock indexes, according to JFK Jr.

However, 2008 was not the beginning. It started a very long time ago.