evening wrap, june 3

market vibes

“Being an engineer (insert your job) is to live in a mean, bare prison cell and regard yourself the sovereign of limitless space... for each engineer has a magician in his soul.” John DeLorean

The OECD slashed its global growth forecasts to 2.9% for 2025, down from 3.1% forecasted in March 2025 and 3.3% in December 2024. Trump tariffs are justifiably to blame, but it’s a moving target, obviously, because the forecast has been falling since last December.

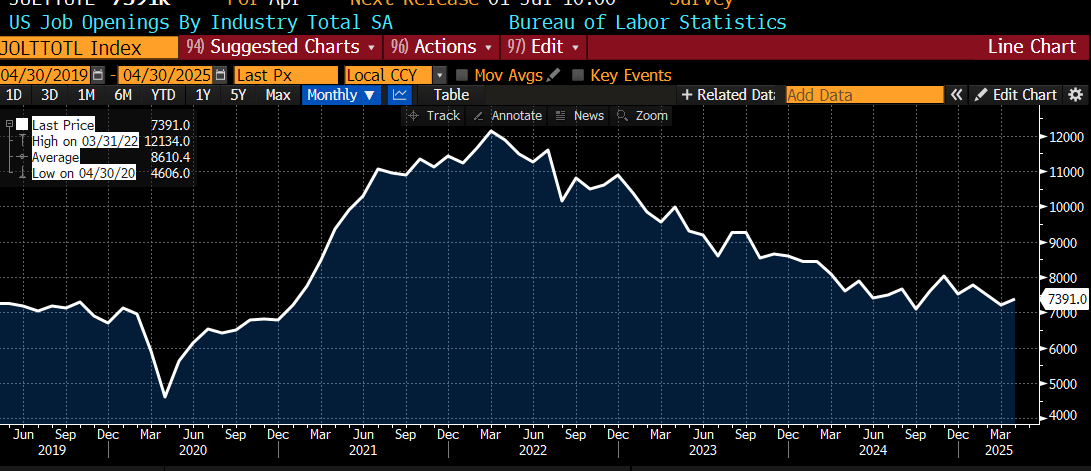

JOLTS layoffs rose to the highest since last September. Durable goods were expected to be +0.2% and came in at -0.5%. Job openings … see the chart below. Ford’s EV sales fell 25% in May. Wards auto sales are down over 2 million units since March 31.

In Trump news, steel tariffs will double tomorrow.

In the markets

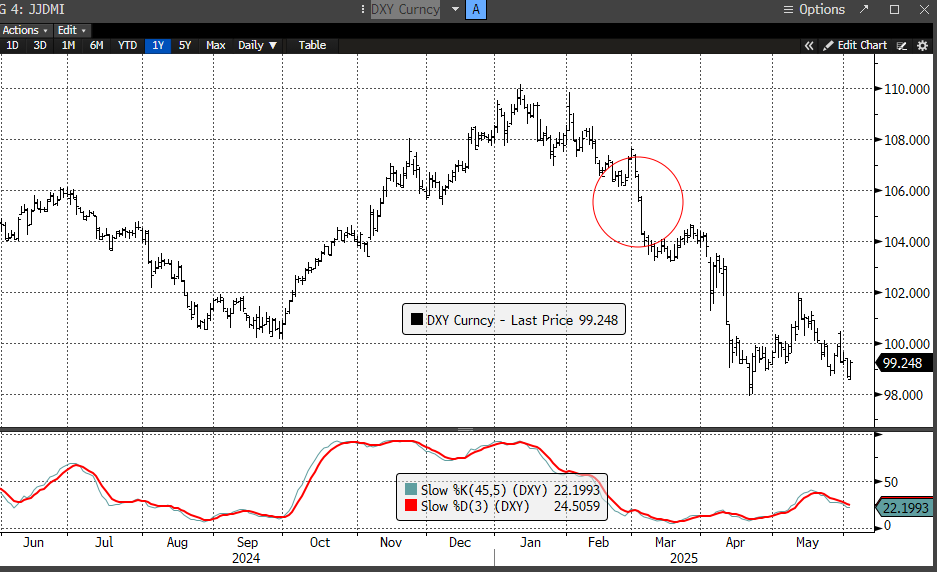

DXY came into NY with a modest bid and continued to rally through the session. The impetus was a weaker yen and euro.

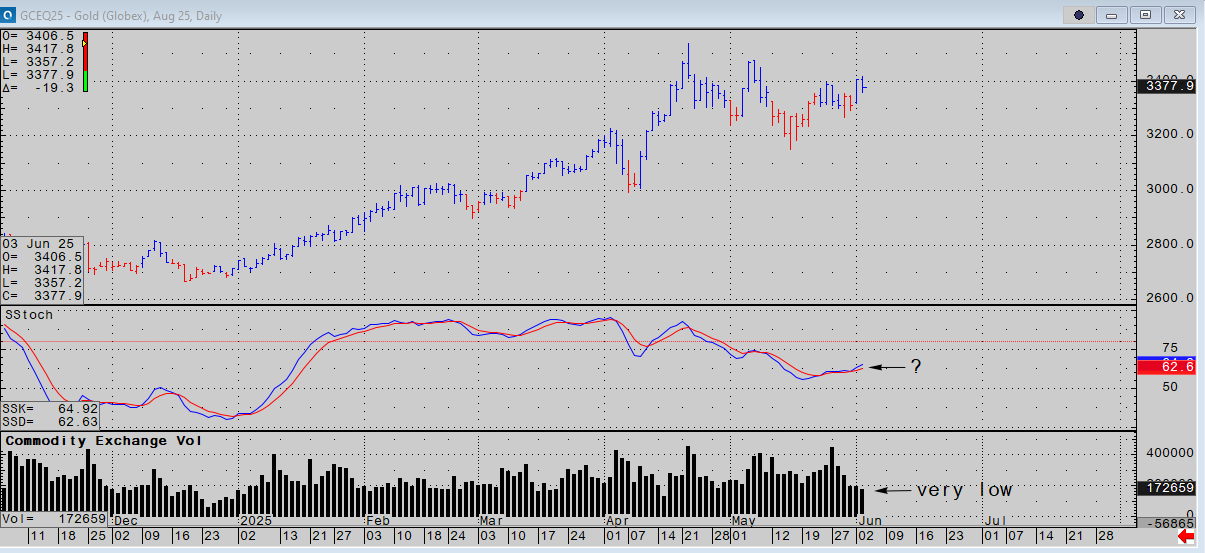

Gold dipped briefly in the morning, held its POC at $3,357, and rallied $20 despite a firmer USD.

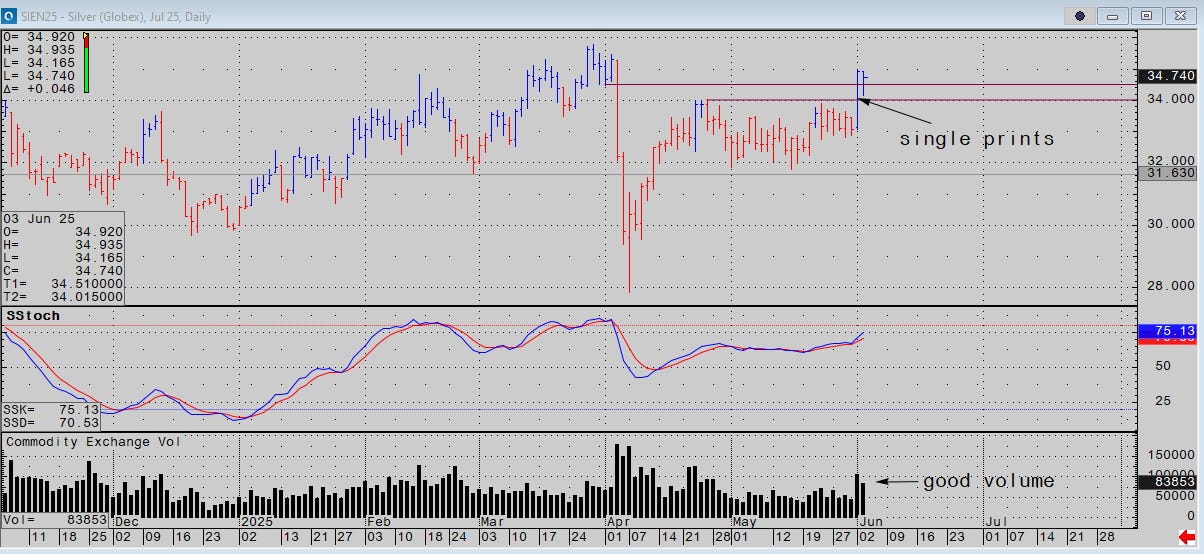

Silver rejected a test of its breakout single prints and closed near the highs. Considering PMs’ usual hypersensitivity to the dollar, sustaining yesterday’s gains is positive. Platinum was equally steady, closing +$10 on the day.

Moving along with some updates; highlighting internal weakness in oil, a fairly deep dive into this extensive range in S&Ps and how to use a slo-stochastic, bitcoin developing a range at the highs that might last a few weeks. And the way it is… in the vibe.