evening wrap, June 1

market vibes

The marquee feature in NY trading on Monday was as usual new all time highs in Stocks. BBG described the $5.00 rally in WTI as the highest in a month. Other markets were typically soporific.

In a note making the rounds on X Goldman Sachs attributes the surprisingly muted rise in oil prices to accelerating “demand destruction” which, they say, is already larger than the post-2011 or 2022 price spikes. Jet fuel, pet-chem, feedstocks, naphtha, propane, gasoline and diesel are pressuring crude. If GS is correct, record high cracks and margins should get hit first.

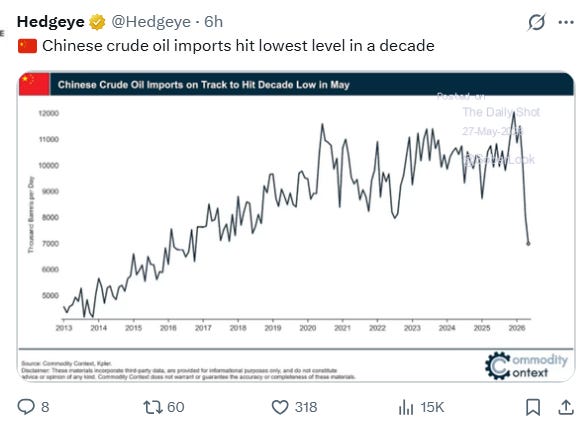

On the NYMEX July RBOB settled at or below $3.10/gallon for a 4th day in a row and reflecting demand for crude in Asia… this post from Hedgeye.

in the markets

This chart is the NYMEX WTI July/August/September butterfly. It says the premium for July over August is 0.20 cents lower than the premium for August over September. On February 27 it settled at $-0.04 and on April 13 it settled at $+1.11. These are internal values that few ever see because they either never look for them or they don’t know they exist. However the trend is clear.

A negative value for the front fly does imply weaker demand in mid-summer. Capacity utilization has been red hot… GS might be correct… that could be tapering off.

The butterfly above is instructive: Backwardation always has the highest price at the front of the curve. Lower forward prices are not the market predicting lower oil prices at those dates. They are an expression of spot demand primarily by refiners lifting spot barrels for daily runs while selling/hedging incoming oil in storage until it gets refined…. buy/sell front to back creates backwardation. Not shortages…

I have shorted more crude bears in backwardation than contango. And I have traded many vertical rallies in contango. Backwardation is generally an operational effect although it can and does occur in extreme shortages. In my opinion it’s not a primary indicator unless there’s a narrative supporting it. This fly is in contango with a shortage narrative. So… there you have it!

This chart is the July/August RBOB (gasoline) front spread pricing demand for prompt gasoline in the NY Harbor. The chart speaks for itself…probing the lows of the March 9 spike high.

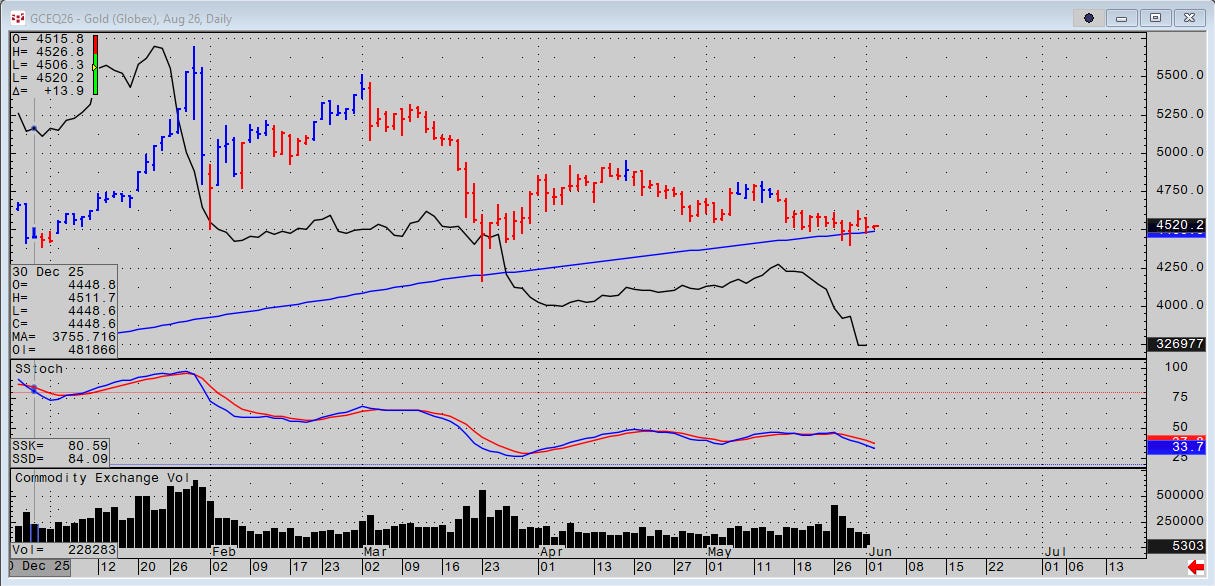

In other markets, bitcoin fell $1000. Gold, silver and platinum have settled essentially unchanged at or within bps of their POCs for 10+ sessions.

August gold (chart below) is an adequate proxy for all precious metals.

Copper stalled in front of a new all time high. Copper is positively correlated with with open interest and stocks…. which are correlated with open interest. This says both markets are long and dominated by a constant marginal imbalance of buying.

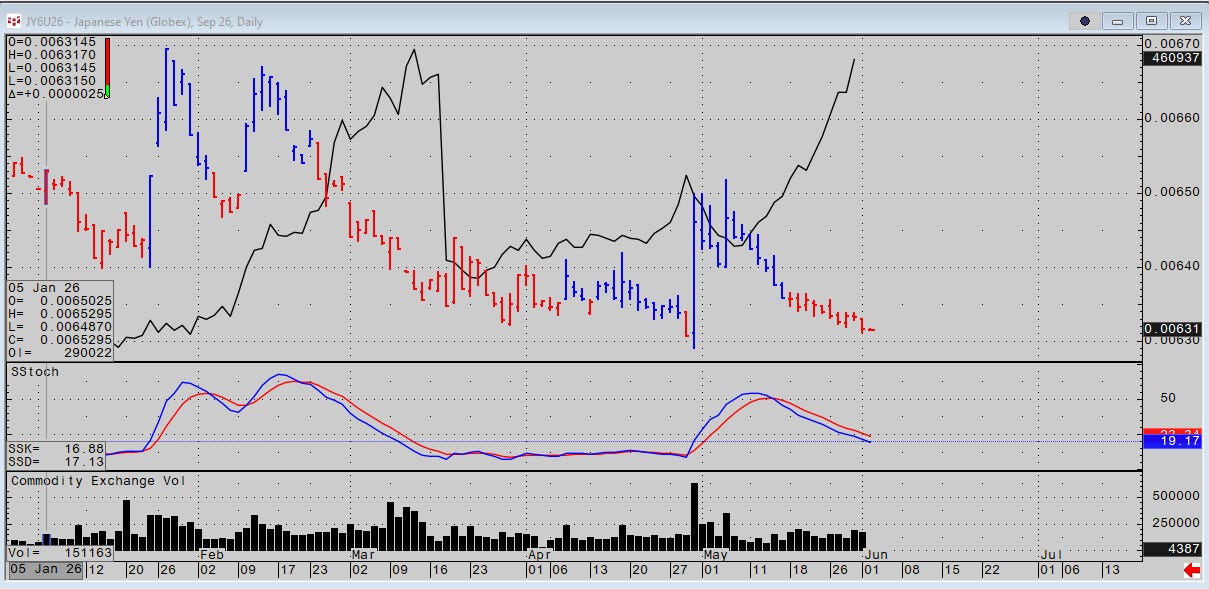

Intervention has not deterred the shorts in Yen futures. We are entering the intervention zone again which may weaken USD and rally gold and silver.

The long bond is heeding the call of its long term POC.

According to Grok as of May 15, 2026 (short interest should be updated tomorrow).

TLT (iShares 20+ Year Treasury Bond ETF):

Short interest ≈19.65% of the public float.Change: +7.97%.

Days to cover: ≈3.8 (based on average daily volume).

marketbeat.com

LQD (iShares iBoxx $ Investment Grade Corporate Bond ETF):

Short interest ≈23.72% of the public float.Change: +26.75%.

Days to cover: ≈2.5.

my vibe

As the conflict in Iran decelerates idle minds and flat P&Ls have returned to America’s most special form of domestic madness which would take an entire note and very risky writing to even list without ruffling and nose-twisting the most jaded reader.

Having said that the freest society in the universe goes to the polls again tomorrow voting in 6 states where primary elections for senators and governors will decide whether or not President Trump’s 117 to 0 unbroken endorsement record will hit new highs. Does anyone in Tehran care about anything else?

Fifteen or 16 states have already chosen primary candidates and by September 15 almost all 50 states including Washington D.C. and territories will choose primary candidates for ALL U.S. House seats, 35 Senate seats, 36 gubernatorial races, and thousands of state and local contests. Bass vs Pratt in LA is the founders’ vision of liberty working as planned.

I must admit, the “war” in the Middle East has become such a mind-numbing bore, political news is a refreshing distraction although I promise not to write about it… much.

Maybe Warsh will shake things up. One can only hope!

leonard cohen the poet quite beautiful…

night all… good luck in asia

JJ

If you like reading market vibes please hit the like button, and type in your e mail below to become a free or paid-up subscriber. Thank you.

Share selectively with friends and colleagues and follow me on X @Alyosha745

Charts and data CQG and Bloomberg… occasional cartoons by Gary Larson

Market vibes is not a registered investment advisor. Comments, thoughts and opinions are entirely those of the author without any representations to accuracy and are for informational use only. Any mention of a particular security, index, derivative, or other instrument is NOT a recommendation to buy, sell, or hold that security, index, derivative, or any other related instrument.

“ As the conflict in Iran decelerates idle minds and flat P&Ls have returned to America’s most special form of domestic madness which would take an entire note and very risky writing to even list without ruffling and nose-twisting the most jaded reader.”

JJ…You Crack Me Up!!!

Worth a year’s subscription just for this Gem!

👊

Did you see… “Powell warns politicized Fed would damage public trust: calls it a ‘stress test’ for democracy.”

Says the Fed head that lowered interest rates 2 months before an election with inflation running high. And the same Fed Head that won’t leave.