double double

market vibes

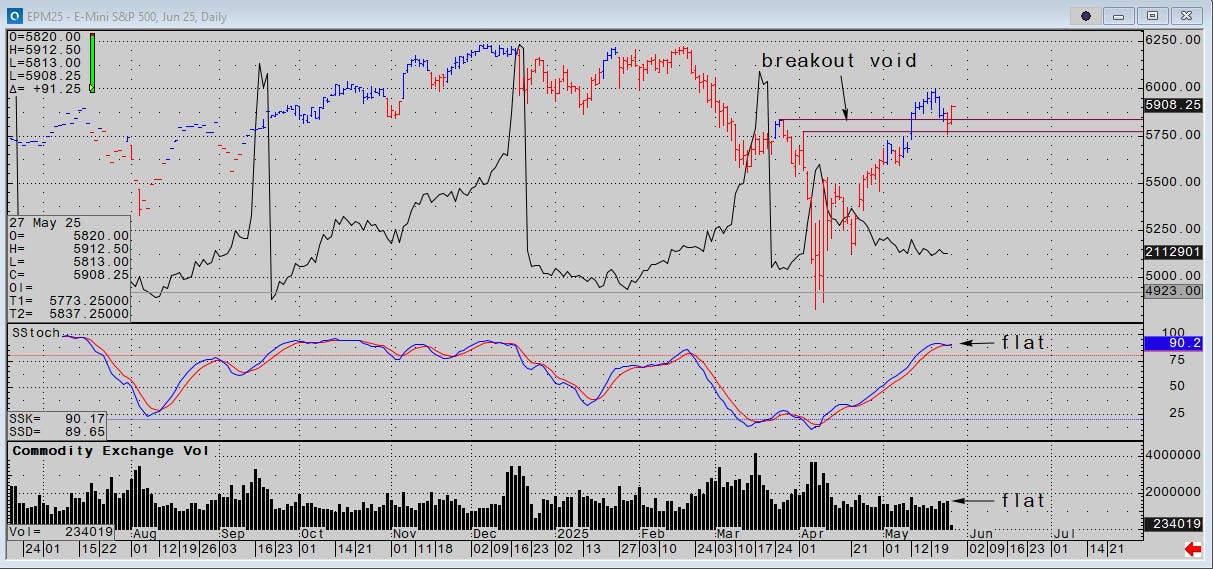

May 27…)

“Knowing when to retreat and having the courage to do it.” The Duke of Wellington when asked to share his most successful tactics in battle.

Data this morning includes Durable Goods at 8:30, plus Housing data from S&P CoreLogic and Consumer Confidence at 10:00. FOMC minutes tomorrow.

In the news

Nvidia reports Q1 tomorrow. NVDA never misses. The bet is by how much they beat, IMO. The stock traded at $86 on April 4 and settled $131 last Friday.

The tax bill heads to the Senate looking more like a mud fence than a beauty queen.

Kobeissi says this on X: In 45 days, Japan's 30-year Government Bond Yield rose a MASSIVE +100 basis points, to a record 3.20%. Over $500 BILLION worth of ‘safe’ 40-year Japanese Government Bonds have lost 20%+ in 6 weeks.” Yikes. Sounds like March 2023…. fwiw, we did survive.

King Charles is in Canada to express his distaste for Trump’s disrespectful designs on the 51st American state. This is not exactly calling out the big guns, but considering the King’s wages, he might as well do some PR for the Commonwealth.

A Southwest plane was struck by lightning while landing in Denver. No injuries.

In the markets

Stocks are up on a tariff reprieve for the EU. The DAX is making a tepid all-time high, and S&Ps are happy to tag along. Bloomberg reported Germany has become the largest net creditor nation in the world (based on 2024 data), surpassing Japan, due to the Teutons’ trade surplus literally levitating out of the earth’s atmosphere last year.

Technically, the S&P handily defended its breakout void last Friday on good volume, and until that area is threatened, I plan to stay off the right-hand side of the ladder. Open interest is still necrotic, indicating the community of bulls might travel comfortably in a pickup truck.

Moving along with bonds, dollars, gold and oil where the starting guns are silent so far and ranges are beginning to grip… Bitcoin clings to its highs alone, and a turn for the worse in the vibe.