cui bono

market vibes

April 14…)

There is either an epidemic misunderstanding of the arithmetic driving the oil crisis (so called) at the Strait of Hormuz or if not that… a deliberate misconstruction of it. Closing the Strait did not make 20 mm bpd of oil that customarily passes through it disappear. It just curtailed it temporarily where it has substantially remained in storage for 6 weeks. For instance: for the first 10 days of March when the Strait was shut, 20 million bpd was redirected to floating storage in the Persian Gulf where it still waits to exit. No barrels were removed from the supply side.

In the next 10 days about 5 million barrels were gradually shut in by Iraq, Kuwait and the UAE. KSA maintained normal rates because they had about 200 mm bbls of onshore storage and 5 mm bpd of pipeline capacity to the Red Sea. However over time perhaps another 200+ mm barrels of cumulative GCC wellhead closures have occurred. That is also latent production that will or must snap back asap.

Saudi Arabia urges trump to lift US blockade

Saudi is currently producing 7.8 million bpd (March actual, with April same or higher) and routing 7 million bpd through the East-West pipeline to Yanbu at the Red Sea. Their pre-war baseline was 9 mbpd at $70/bbl or $630 million/day.

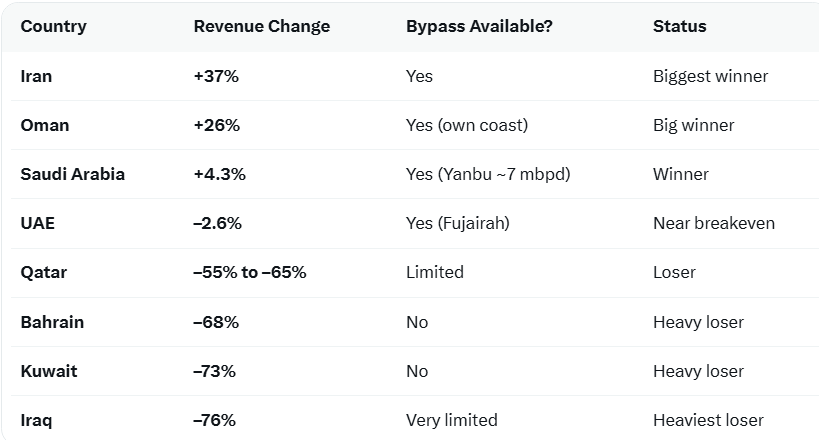

Now they are exporting 7 mbpd at $110 to $120+/bbl … which, including OSP premiums, equals $750 to $840 million/day. Better said a windfall daily operating gain of $100 to $200 mm dollars. And they are sitting on a treasure chest of 200 million barrels in storage. See below courtesy of Grok a snapshot of GCC winners and losers to date.

Iran is the biggest winner followed by Oman and KSA.

The only real losers are Bahrain, Kuwait and Iraq. The combined total loss of barrels due to shut-ins for these three countries is estimated at 188 – 214 million barrels lost since March 1. With KSA’s 200 mm barrels accumulated in onshore storage the absolute loss of barrels to the market is almost nil… not quite but directionally very close.

Therefore there’s very little pressure from the GCC winners to lift the Iranian blockade (except Iran). In fact as the oilprice.com article implies KSA would rather keep things as they are! I am beginning to think Trump might like that, too, or at least be ambivalent.

In other news ADP reports on jobs this morning but the employment situation seems more AI related than data dependent. NVDA, META and Google have been ripping higher. PPI today with core expected 4.2 % vs 3.9% last month (oil prices).

in the markets

For the time being oil prices are where they want to be. May WTI bounced off its point of control on light volume and rising open interest while following a flaccid response to the US blockade yesterday. The fact is for all the hubbub and hair pulling and air-to-air combat… prices haven’t moved at all since March 9 and… the range has grown ever more docile.

We have APIs at 4 PM and DOEs tomorrow and I suspect inventories are going to keep rising. When the armada of VLCCs arrive they’ll draw. That should be interesting for spreads. Next chart: