bittersweet

market vibes

Friday February 13…)

In the news

US CPI data was expected mixed or flat or slightly higher this morning and MoM came in a dovish 0.2% vs 0.3% expected. Everything else on consensus.

In oil, the UK’s Tony Blair is considering a restart in the North Sea. Kuwait plans to increase bpd to 4M by 2035 (3.2M bpd today). Chris Wright thinks Venezuela can “dramatically increase production of oil and gas this year (I agree).” Canada is actively growing its export capacity to the west coast. Trump foresees several weeks of continuing negotiations with Iran. Concurrently global demand growth is expected to decline (IEA yesterday).

Bloomberg: “Nearly 90% of the economic burden from tariffs in 2025 was borne by US companies and consumers, according to a new study by economists at the Federal Reserve Bank of New York”… LOL… which is why companies from all over the world are spending billions to come to America and build businesses locally. They can’t wait to bear the same burdens!

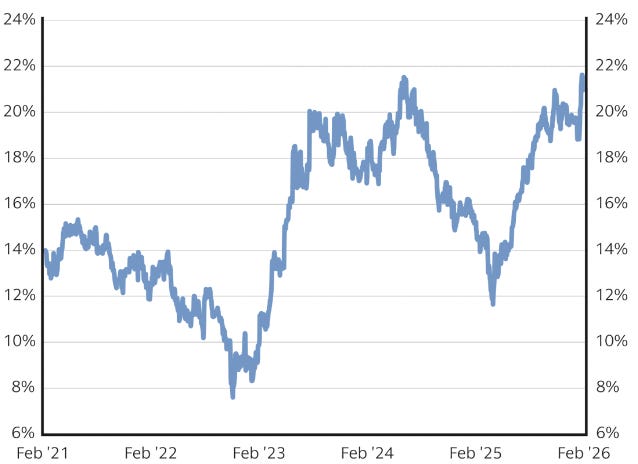

GS posted this chart to subscribers of their daily note. A year ago the Mag 7 had the exact same weighting in American portfolios as of Feb 5, 2026. This seems counterintuitive considering the weakest link in the equity markets is AI. But… there it is.

in the markets

April gold is back above $5,000. I wouldn’t bet the farm on it staying there but development is beginning to look positive. Rising OI means we saw responsive buying on the dip yesterday and there is immense headroom to add length in futures.

It is possible to see a (blue bar) 1-bar false positive today which seems highly likely if we trade above $5,144. This red blue red blue DMI debate implies indecision. Still looking for a POC. Low volume despite yesterday’s whoopsie implies continuing deceleration.

Silver is still liquidating and decelerating.