gold is talking

September 24…)

“If I had my choice I would kill every reporter in the world, but I am sure we would be getting reports from Hell before breakfast.” William Tecumseh Sherman

Philly Fed manufacturing at 8:30 this morning expected to improve to -9 from -25. S&P housing data at 9:00 expected unch. Consumer confidence and Richmond Fed at 10.

In the news

A full cycle of escalation in Lebanon, replete with glossy color photographs of hell, video clips of panicky innocents and reports America is adding to its troop buildup in Israel.

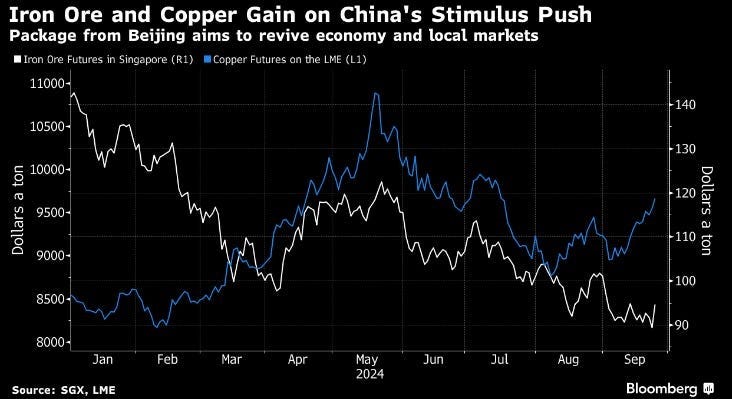

China deployed a stimulus package that may include buying up to $113 billion local equities and a high focus on real estate lowering down payments on 2nd homes to 15% from 25 %. The PBOC will cover 100% of loans for local governments buying unsold homes, up from 60%. It sounds like they mean business this time.

in the markets

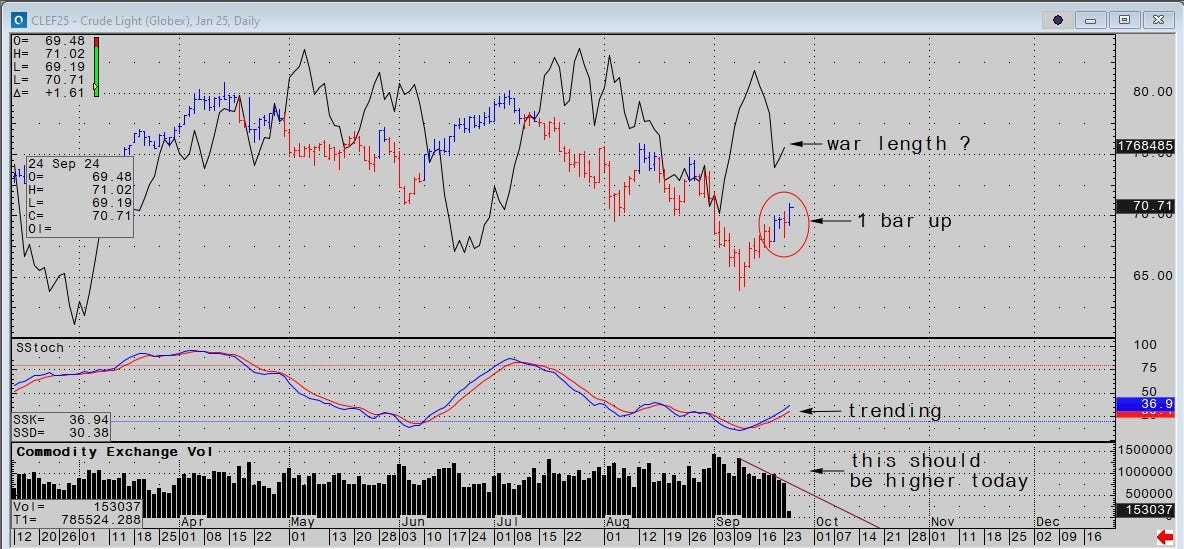

Oil is up on Lebanon and China. There is a potential mid-trend 1 bar up encircled that won’t confirm until settlement. If that happens and I were short, which I am not, I’d cover. Of all the boogie men fanning the fires in oil, war is the real game changer. Rate cuts and stimulus will help but not for a while. The reality of war today is it’s a measured enterprise that makes money for all sides. No one wants peace.

Copper was technically well positioned for this news from China. Zinc is making new monthly and quarterly highs. If they go higher, they’ll lend a hand to the whole metals sector including precious metals, I think.

In other markets a new new dynamic is unfolding.

Keep reading with a 7-day free trial

Subscribe to market vibes to keep reading this post and get 7 days of free access to the full post archives.